Tag: Student perspectives

Student perspectives: Regional Sensitivity Analysis

A post by Cecina Babich Morrow, PhD student on the Compass programme.

Introduction

Sensitivity analysis seeks to understand how much changes in each input affect the output of a model. We want to be able to determine how variation in a model’s output can be attributed to variations in its input. Given the high amount of uncertainty present in most real-world modelling settings, it is crucial to understand the magnitude of this uncertainty’s impact on model results. Knowing how sensitive a model is to a particular parameter can help guide modellers in prioritising what level of precision is needed in estimating that parameter in order to produce valid results. Sensitivity analysis thus serves as a vital tool for modellers in numerous fields, allowing them to assess robustness and to identify key drivers of uncertainty. By systematically analysing the relative amount of influence that each input parameter has on the output, sensitivity analysis reveals which parameters have the greatest impact on the results.

By identifying these critical parameters, stakeholders can prioritize investments in data collection, parameter estimation, and uncertainty reduction. This targeted approach ensures that efforts are concentrated where they will have the most significant impact.

Why use Regional Sensitivity Analysis?

In this blog post, I will focus on one particular sensitivity analysis method that I have been using in my project so far to help understand the sensitivity of an output decision to input parameters which affect that decision. Regional Sensitivity Analysis (RSA) was developed in the field of hydrology, but has widespread applications in environmental modelling, disease modelling, and beyond.

My research focuses on environmental decision-making, so I frequently deal with models that output a decision that can take on one of several discrete values. For example, consider trying to make a decision about what to wear based on the weather. To make our decision, we use three input parameters about the weather: temperature, humidity, and wind speed. Then, our decision model can output one of three decisions: (1) stay home, (2) leave the house with a jacket, (3) leave the house without a jacket. We might then be interested in how sensitive our model is to each of our three weather-related input parameters to understand how much each one contributes to uncertainty in our ultimate decision. In this type of setting, we need to use a sensitivity analysis method that can handle continuous inputs, e.g. temperature, in conjunction with a discrete output, e.g. our decision.

For settings such as these where the inputs of our model are continuous and the outputs are discrete, RSA, also referred to as Monte Carlo filtering, is a potential method of sensitivity analysis [1]. RSA aims to identify which regions of input space corresponding to specific values in the output space [2, 3]. Originally, the method was developed in the field of hydrology for cases where the output variable is binary, or made such by applying a threshold. It has since been extended by splitting the parameter space into more than two groups [3, 4]. RSA is well-suited to sensitivity analysis in the case where the output variable is categorical [5].

RSA is fundamentally a Bayesian approach. First, prior distributions are assigned to the input parameters. The model is then run multiple times, sampling input parameters from these priors, and recording the resulting output values. By analysing the relationship between input uncertainties and output uncertainties, RSA identifies which parameters significantly affect the model’s predictions.

How does RSA work?

We will present the mathematical formalisation of RSA in a setting where we have a discrete output variable

![\mathbf{x} = [x_1, x_2, \ldots, x_d]](https://s0.wp.com/latex.php?latex=%5Cmathbf%7Bx%7D+%3D+%5Bx_1%2C+x_2%2C+%5Cldots%2C+x_d%5D&bg=ffffff&fg=000000&s=0 "\mathbf{x} = [x_1, x_2, \ldots, x_d]")

Then, RSA compares the empirical conditional cumulative distribution functions (CDFs)

")

= F(x_i | y_1) = \ldots = F(x_i | y_m)")

The difference between these CDFs can be measured using several possible sensitivity indices. Typically, the Kolmogorov-Smirnov (KS) statistic is applied over all possible values of

![\text{stat}_{j,k} [KS(x_i)] = \text{stat}_{j,k} \left[\max_{x_i} \left \lvert F_{x_i | y_j} (x_i | y = y_j) - F_{x_i | y_k} (x_i | y = y_k) \right \rvert\right]](https://s0.wp.com/latex.php?latex=%5Ctext%7Bstat%7D_%7Bj%2Ck%7D+%5BKS%28x_i%29%5D+%3D+%5Ctext%7Bstat%7D_%7Bj%2Ck%7D+%5Cleft%5B%5Cmax_%7Bx_i%7D+%5Cleft+%5Clvert+F_%7Bx_i+%7C+y_j%7D+%28x_i+%7C+y+%3D+y_j%29+-+F_%7Bx_i+%7C+y_k%7D+%28x_i+%7C+y+%3D+y_k%29+%5Cright+%5Crvert%5Cright%5D+&bg=ffffff&fg=000000&s=0 "\text{stat}_{j,k} [KS(x_i)] = \text{stat}_{j,k} \left[\max_{x_i} \left \lvert F_{x_i | y_j} (x_i | y = y_j) - F_{x_i | y_k} (x_i | y = y_k) \right \rvert\right]")

where

For instance, consider the following situation with an input parameter ")

")

")

")

Figure 1. Visualisation of RSA using a summary statistic of the KS statistic as a sensitivity index. The blue, green, and red distributions are the empirical conditional CDFs ")

As an alternative to using the KS statistic, we can instead apply a statistic to spread, i.e. the area between the CDFs:

![\text{stat}_{j,k} [\text{spread}(x_i)] = \text{stat}_{j,k} \left[ \int_{-\infty}^\infty \max \left(F_{x_i | y_j} (x_i | y = y_j), F_{x_i | y_k} (x_i | y = y_k)\right) dx_i - \int_{-\infty}^\infty \min \left(F_{x_i | y_j} (x_i | y = y_j), F_{x_i | y_k} (x_i | y = y_k)\right) dx_i \right]](https://s0.wp.com/latex.php?latex=%5Ctext%7Bstat%7D_%7Bj%2Ck%7D+%5B%5Ctext%7Bspread%7D%28x_i%29%5D+%3D+%5Ctext%7Bstat%7D_%7Bj%2Ck%7D+%5Cleft%5B+%5Cint_%7B-%5Cinfty%7D%5E%5Cinfty+%5Cmax+%5Cleft%28F_%7Bx_i+%7C+y_j%7D+%28x_i+%7C+y+%3D+y_j%29%2C+F_%7Bx_i+%7C+y_k%7D+%28x_i+%7C+y+%3D+y_k%29%5Cright%29+dx_i+-+%5Cint_%7B-%5Cinfty%7D%5E%5Cinfty+%5Cmin+%5Cleft%28F_%7Bx_i+%7C+y_j%7D+%28x_i+%7C+y+%3D+y_j%29%2C+F_%7Bx_i+%7C+y_k%7D+%28x_i+%7C+y+%3D+y_k%29%5Cright%29+dx_i+%5Cright%5D&bg=ffffff&fg=000000&s=0 "\text{stat}_{j,k} [\text{spread}(x_i)] = \text{stat}_{j,k} \left[ \int_{-\infty}^\infty \max \left(F_{x_i | y_j} (x_i | y = y_j), F_{x_i | y_k} (x_i | y = y_k)\right) dx_i - \int_{-\infty}^\infty \min \left(F_{x_i | y_j} (x_i | y = y_j), F_{x_i | y_k} (x_i | y = y_k)\right) dx_i \right]")

where

Higher values of either sensitivity index for a given input parameter

")

")

Figure 2. Comparison of sensitivity of a model to two input parameters, ")

Extensions of RSA

One notable limitation of RSA, identified since its inception [2], is its inability to handle parameter interactions. A zero value of the sensitivity index is a necessary condition for insensitivity, but it is not sufficient [2, 5]. Inputs that contribute to variation in the model output only through interactions can have the same univariate conditional CDFs, and thus RSA cannot properly identify their impact on model output. For theoretical examples, see Fig. 1 of [2] and Example 6 of Section 5.2.3 in [1]. In our toy example, we may have a decision model where the output decision is not particularly sensitive to temperature or humidity on their own, but it may be very sensitive to an interaction between these two parameters since their combined effects impact how warm or cool the weather actually feels.

In situations such as these where interactions between input variables may matter more than each variable on its own, RSA can be useful for ranking, but it cannot be used for screening, another goal of sensitivity analysis aiming to identify variables with little to no influence on output variability[1, 5]. To address this limitation, RSA can be augmented with machine learning methods such as random forests and density estimation trees [6]. Spear et al. performed a sensitivity analysis of a dengue epidemic model to demonstrate how these tree-based models can augment RSA [6].

First, the authors performed RSA in its original form, using the KS statistic to examine the difference between the univariate CDFs. Then, they used random forest analysis to classify model runs into the various output values. Then, a measure of variable importance, such as Gini impurity, was used to rank the input parameters in terms of their influence on the model output [6]. Random forest allows for the incorporation of the effects of variable interactions in ranking the importance of each parameter. By comparing the parameter ranking resulting from RSA with that from the random forest, they identified parameters which impacted the output through interaction. Finally, they used density estimation trees to help identify regions of parameter space corresponding to particular output values. Density estimation trees are the analogue of classification and regression trees, instead attempting to estimate the probability density function that gave rise to a particular region of output space [7]. By applying density estimation trees as part of the sensitivity analysis, Spear et al. were able to examine the effects of scale on sensitivity, identifying parameters which may be relatively unimportant when ranking across the entire parameter subspace, but are highly influential in small subspaces.

Further research such as this highlights the benefits of combining multiple sensitivity analysis methods in order to gain a full picture of how model inputs affect uncertainty in the output.

Conclusions

Hopefully this blog has been an informative crash course in regional sensitivity analysis! Note that the visualisations in this post have been created using the SAFEpython toolbox [8]. If you have any questions or comments, please feel free to get in touch at cecina.babichmorrow@bristol.ac.uk.

References

[1] A. Saltelli, Global sensitivity analysis: the primer. Wiley, 2008. [Online]. Available: https://onlinelibrary.wiley.com/doi/book/10.1002/9780470725184

[2] R. Spear and G. Hornberger, “Eutrophication in peel inlet—II. identification of critical uncertainties via generalized sensitivity analysis,” Water Research, vol. 14, no. 1, pp. 43–49, 1980. [Online]. Available: https://www.sciencedirect.com/science/article/pii/0043135480900408

[3] J. Freer, K. Beven, and B. Ambroise, “Bayesian estimation of uncertainty in runoff prediction and the value of data: An application of the GLUE approach,” Water Resources Research, vol. 32, no. 7, pp. 2161–2173, 1996. [Online]. Available: https://onlinelibrary.wiley.com/doi/abs/10.1029/95WR03723

[4] T. Wagener, D. P. Boyle, M. J. Lees, H. S. Wheater, H. V. Gupta, and S. Sorooshian, “A framework for development and application of hydrological models,” Hydrology and Earth System Sciences, vol. 5, no. 1, pp. 13–26, 2001. [Online]. Available: https://hess.copernicus.org/articles/5/13/2001/

[5] F. Pianosi, K. Beven, J. Freer, J. W. Hall, J. Rougier, D. B. Stephenson, and T. Wagener, “Sensitivity analysis of environmental models: A systematic review with practical workflow,” Environmental Modelling & Software, vol. 79, pp. 214–232, 2016. [Online]. Available: https://linkinghub.elsevier.com/retrieve/pii/S1364815216300287

[6] R. C. Spear, Q. Cheng, and S. L. Wu, “An example of augmenting regional sensitivity analysis using machine learning software,” vol. 56, no. 4, p. e2019WR026379. [Online]. Available: https://onlinelibrary.wiley.com/doi/abs/10.1029/2019WR026379

[7] P. Ram and A. G. Gray, “Density estimation trees,” in Proceedings of the 17th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, pp. 627–635. [Online]. Available: https://dl.acm.org/doi/10.1145/2020408.2020507

[8] F. Pianosi, F. Sarrazin, and T. Wagener, “A Matlab toolbox for global sensitivity analysis,” Environmental Modelling & Software, vol. 70, pp. 80–85, 2015. [Online]. Available: https://linkinghub.elsevier.com/retrieve/pii/S1364815215001188

Student Perspectives: The trade-off between sample size and number of trials in meta-analysis

A post by Xinrui Shi, PhD student on the Compass programme.

Introduction

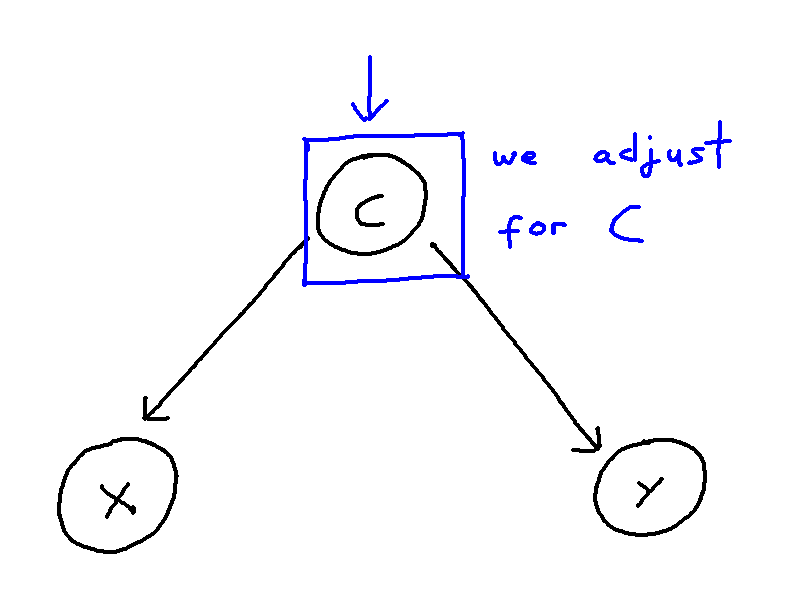

Meta-analysis is a widely used statistical method for combining evidence from multiple independent trials that compare the same pair of interventions [1]. It is mainly used in medicine and healthcare but has also been applied in other fields, such as education and psychology. In general, it is assumed that there is a numerical measure of effectiveness associated with each intervention, and the goal is to estimate the difference in effectiveness between the two interventions. In medicine, this difference is termed the relative treatment effect. We assume that relative effects vary across trials but are drawn from some shared underlying distribution. The objective is to estimate the mean and standard deviation of this distribution, which we denote by $d$ and $\tau$ respectively; $\tau$ is referred to as the heterogeneity parameter.

In medical trials, patients are randomly allocated to one of the two treatment options, and their subsequent health outcomes are monitored. Each trial then provides an observation of the relative treatment effect in that trial. Meta-analysis uses these observations to estimate the mean $d$ and variance $\tau^2$ of the distribution of relative effects. In this work, we are interested in understanding what conditions maximise the precision of these pooled estimates.

It is well-known that the precision of meta-analysis can be improved by either increasing the number of observations or improving the precision of individual observations. Both approaches, however, require more participants to be included in the meta-analysis. To understand the relative importance of these factors, we constrain the total number of participants to a fixed value. Then, if more trials are conducted to generate additional observations, each trial will necessarily include fewer participants, thereby reducing the precision of each individual observation. Given this trade-off between the precision of observations and their quantity, we ask: how should participants be optimally partitioned across trials to achieve the most precise estimates?

Meta-analysis background

Model

Suppose there are two treatments for a disease, labelled $T_1$ and $T_2$, and we want to know which one is more effective. There are a total of $n$ patients across $M$ trials, and patients in each trial are randomly allocated to one of the two treatments. We write $n_{ij}$ for the number of patients assigned to treatment $T_j$ in trial $i\in \{ 1,\ldots,M \}$.

Outcomes refer to a patient’s health status after treatment. Here, we assume a binary outcome, either recovered or not recovered. A natural measure of the effectiveness of a treatment is the probability of recovery. Let $p_{ij}$ denote the probability of recovery after receiving treatment $T_j$ in trial $i$, and $X_{ij}$ the number of these patients who recover. We assume that outcomes are independent across patients. It then follows that $X_{{ij}}$ has a Binomial distribution,

\[eq(1):\quad X_{{ij}} \sim \text{Binomial}(n_{ij}, p_{ij}).\]

Due to differences in trial populations and procedures, the recovery probabilities are not assumed to be the same across trials. Instead, we assume the exchangeability of relative effects.

We model relative treatment effects on the continuous scale. Therefore, we transform $p_{ij}$ to its log-odds,

\begin{equation*}

\quad Z_{ij} := \text{logit}(p_{ij}) = \log \frac{p_{ij}}{1-p_{ij}}

\label{eq:def_Zij}

\end{equation*}

and define the trial-specific relative treatment effect, $\Delta_{i,12}$, as the log odds ratio (LOR) between the two treatments in this trial,

\begin{equation}\label{eq:LOR}

eq(2):\quad \Delta_{i,12}:= Z_{i2}- Z_{i1}=\log \frac{p_{i2}(1-p_{i1})}{p_{i1}(1-p_{i2})}.

\end{equation}

In words, $\Delta_{i,12}$ represents the effect of $T_2$ relative to $T_1$ in the $i$-th trial; $\Delta_{i,12}>0$ indicates that $T_2$ is more effective than $T_1$.

The random effects (RE) model assumes that the treatment effects vary across trials,

\begin{equation}

eq(3):\quad \Delta_{i,12}\sim \text{Normal}(d_{12},\tau^2),

\label{eq:normal_assump2}

\end{equation}

where $d_{12}$ represents the true mean of relative treatment effects between $T_1$ and $T_2$. The fixed effect (FE) model is a special case of the RE model, in which the relative treatment effects in all trials are assumed to be equal, i.e, $\tau=0$ and $\Delta_{i,12} \equiv d_{12}$ for all $i \in \{1,\ldots,M\}$.

Data

To achieve the primary goal of estimating $d_{12}$ and $\tau$, we first derive expressions for the relative treatment effects in each trial from the available data.

We write $r_{ij}$ for the realisation of the random variable $X_{ij}$. The observed relative treatment effect in the $i$-th trial is then

\[

\hat{\Delta_{i,12}} = \log\frac{n_{i2}(n_{i1}-r_{i1})}{n_{i1}(n_{i2}-r_{i2})}.

\]

It can be shown for our binomial model that, as the numbers of patients $n_{i1}$ and $n_{i2}$ grow large, the distribution from which $\hat{\Delta_{i,12}}$ is sampled is asymptotically normal, centred on the true trial-specific effect $\Delta_{i,12}$ and with a sampling variance $\sigma_i^2$ that can be explicitly expressed in terms of $n_{i1}$, $n_{i2}$, and the unknown parameters $p_{i1}$ and $p_{i2}$. The true variance $\sigma^2_i$ is thus unknown, but can be estimated as follows,

\begin{equation}

eq(4): \quad \hat{\sigma^2_i} = \frac{1}{r_{i1}} +\frac{1}{n_{i1}-r_{i1}} +\frac{1}{r_{i2}} +\frac{1}{n_{i1}-r_{i2}}.

\end{equation}

In many practical applications of meta-analysis, it is only the relative treatment effects and their estimated variance that are reported in individual studies, and not the raw data. Hence, meta-analysis often starts by treating $\hat{\Delta_{i,12}}$ and $\hat{\sigma^2_i}$ as the primary data from the $i$-th trial. The goal is then to aggregate data across trials to estimate $d_{12}$, the true treatment effect.

Estimating model parameters

The estimate of $d_{12}$ is given by the weighted mean of estimates from each trial,

\begin{equation}\label{eq:d-hat}

eq(5): \quad\hat{d}_{12} = \frac{\sum_{i=1}^M w_i \hat{\Delta_{i,12}}} {\sum_{i=1}^M w_i }.

\end{equation}

The usual choice of the weight $w_i$ is the inverse of the variance estimate associated with trial $i$. For the FE model this is $w_i = \hat{\sigma_i^{-2}}$, and for the RE model, $w_i = 1/(\hat{\sigma_i^{2}}+\hat{\tau^2})$; here, $\hat{\sigma_i^2}$ is given in (4) and $\hat{\tau^2}$ in (7) below. The choice of inverse variance weights minimises the variance of the estimator $\hat{d_{12}}$, as can be shown using Lagrange multipliers. Substituting these weights in (5) and computing the variance, we obtain that

\begin{equation}

\label{eq:optimised_var}

eq(6): \quad \mbox{Var}(\hat{d_{12}}) =\frac{1}{M} \left( \frac{1}{M} \sum_{i=1}^M \frac{1}{\mbox{Var}(\hat{\Delta_{i,12}})} \right)^{-1},

\end{equation}

where $\mbox{Var}(\hat{\Delta_{i,12}})$ $=\hat{\sigma^2_i}$ in the FE model and $\hat{\sigma^2_i}+\hat{\tau^2}$ in the RE model, as noted above. In words, the variance of the meta-analysis estimate of the treatment effect is the scaled (by $1/M$) harmonic mean of the variances from the individual trials.

One class of methods for estimating the unknown heterogeneity parameter, $\tau$, is the so-called `method of moments’ [2], which equates the empirical between trial variance with its expectation under the random effects model. The widely-used DerSimonian and Laird (DL) [1] estimator is a specific implementation of the method of moments given by

\begin{equation}

eq(7): \quad \hat{\tau^2} = \frac{\sum_{i=1}^M\hat{\sigma_i^{-2}}\left(

\hat{\Delta_{i,12}} – \frac{\sum_{l=1}^M \hat{\sigma_l^{-2}}\hat{\Delta_{l,12}}}{\sum_{l=1}^M \hat{\sigma_l^{-2}}}

\right)^2 – (M-1)}{\sum_{i=1}^M\hat{\sigma_i^{-2}} – \frac{\sum_{i=1}^M\hat{\sigma_i^{-4}}}{\sum_{i=1}^M\hat{\sigma_i^{-2}}}}.

\label{eq:DL_tau2}

\end{equation}

The right-hand side of the above formula can be negative, in which case $\hat{\tau^2}$ is set to zero.

Optimal partitioning of patients

Our aim is to determine the optimal allocation of participants across trials that yields the most precise meta-analysis estimates. We first address this analytically by seeking the allocation that minimises the variance of $\hat{d_{12}}$ in an asymptotic regime in which the number of patients tends to infinity. We complement the theoretical analysis with simulations over a wide range of numbers of patients.

Theoretical findings

To obtain analytic results, we make two simplifying assumptions. First, we assume that each trial, and each treatment within each trial, involves the same number of participants, i.e., $n_{ij}=\frac{n}{2M} \hspace{3pt}$ for all $\{i,j\}$. Then, we consider a limit as the total number of participants, $n$, as well as the number in each trial, $n/M$, tend to infinity. In this limiting regime, the observed number of recoveries, $r_{ij}$, in each arm and trial, satisfies $r_{ij}=np_{ij}/2M$, where $p_{ij}$ is the true probability of recovery. substituting this in (4) yields

\begin{equation} \label{eq:var_est_symm}

eq(8): \quad \hat{\sigma}^2_i = \frac{2Ma_i}{n}, \mbox{ where } a_i=\frac{1}{p_{i1}}+\frac{1}{1-p_{i1}}+\frac{1}{p_{i2}}+\frac{1}{1-p_{i2}}.

\end{equation}

By approximating the asymptotic distribution of $\hat{d_{12}}$, the problem of minimising the variance of $\hat{d}_{12}$ is transferred into to the following optimisation problem:

\begin{equation*}

\max_{M, \tau} \left[\sum_{i=1}^M \frac{1}{2Mna_i+\tau^2}\right], \quad a_i := \frac{1}{p_{i1}(1-p_{i1})}+\frac{1}{p_{i2}(1-p_{i2})}.

\label{eq:opt_problem_asymtotic}

\end{equation*}

Fixed effects: Under the FE model, $\tau=0$ and the optimization problem reduces to

\[

\max_M \left[\frac{1}{2M}

\sum_{i=1}^M \frac{1}{a_i}

\right].

\]

Assuming the values of $a_i$ are roughly of the same order of magnitude, we approximate

$$\sum_{i=1}^M \frac{1}{a_i} \approx \frac{M}{\bar{a}}, \quad \bar{a} := \frac{1}{M}\sum_{i=1}a_i.$$

Hence, the objective function is independent of $M$, indicating that the partitioning of participants does not influence the precision of estimation. This result aligns with our expectation, as, in the FE model, we are only estimating the mean of the distribution and not the variance.

Random effects: In the RE model, we must also estimate the between-trial variance $\tau^2$, which is working in progress.

Empirical findings

To assess whether findings based on asymptotic performance hold in practical scenarios, we conduct a simulation study involving a total of 20,000 participants. We vary the number of trials, $M$, in unit steps from 1 to 200. The number of participants assigned to each treatment in each trial, $n_{i1}=n_{i2}$, therefore varies from 10,000 to 50. We set the true relative treatment effect equal to $d_{12}=0.05$, with heterogeneity parameter $\tau=0.1$ for the RE model.

Data simulation: For each $M$ (and corresponding $n_{i1}=n_{i2}$), we sample trial-specific relative effects $\Delta_{i,12}$ from Equation (3). To construct the corresponding recovery probabilities, we sample $p_{i,1}$ from a standard uniform distribution and calculate $p_{i,2}$ by rearranging Equation (2) to give

\[

p_{i,2} = \frac{p_{i,1}e^{\Delta_{i,12}}}{1 + p_{i,1}(e^{\Delta_{i,12}}-1)}.

\]

Finally, we simulate the number of recovered patients, $r_{ij}$, from the binomial distribution in Equation (1). This yields the simulated data set,

$$\mathcal{D}= \left\{

(r_{i,j},n_{i,j}): i \in\{1,\ldots,M\}, j\in\{1,2\}

\right\},$$

which we use to estimate the model parameters via Equations (5) and (7).

For each $M$, we repeat the simulation 100 times and calculate the median and the interquartile range (IQR) of the estimates $\hat{d_{12}}$ and $\hat{\tau}$.

Estimation of $\hat{d}_{12}$ in FE model: The following figure shows the median and IQR of the estimated mean relative treatment effect $\hat{d}_{12}$ and its standard error for the FE model. As $M$ increases, the standard error on $\hat{d}_{12}$ increases while its estimate fluctuates around the true parameter value. This indicates that the FE estimate $\hat{d}_{12}$ becomes less precise as participants are partitioned into more trials (with fewer participants in each).

Estimation of $\hat{d}_{12}$ in RE model: The following figure shows the estimated mean and standard error of the relative treatment effect in the RE model. As before, the estimated mean is not affected by the number of trials. The standard error exhibits an initial sharp increase from $M=1$ (one large trial) and then decreases until the number of trials reaches approximately 40. After this, the standard error remains almost fixed. This indicates that for more than one trial, the estimated mean relative treatment effect is more precise when participants are partitioned into more trials.

Estimation of $\hat{\tau}$ in RE model: The following figure shows the estimated mean and standard error of the heterogeneity estimate $\hat\tau$ in the RE model. For very few trials ($M<6$), heterogeneity is underestimated (at $M=1$ this is zero since there can be no variation between one trial). As the number of trials increases, $\hat\tau$ fluctuates about its true value but with increasing variation (IQR). Beyond $M=1$ (where the standard error is necessarily zero), the standard error on $\hat{\tau}$ decreases with increasing $M$ up to approximately $M=10$, at which point it increases again. This suggests that, for the scenario simulated in this study, the precision of the heterogeneity estimate is optimal when participants are partitioned into about 10 trials (with $n_{i1}=n_{i2}=1000$).

Summary: Even with a large number of participants, the theoretical results only hold for a smaller number of trials. This is because the number of participants per trial decreases when partitioning into more trials.

Future work: As our simulation only extended to 200 trials, it did not investigate scenarios with small numbers of participants per trial. In future work we will explore these more extreme scenarios, taking the number of trials to its maximum (i.e. with one participant per treatment in each trial). We will also investigate the generalizability of our findings to other parameter values ($d_{12}$ and $\tau$), continuous rather than binary outcomes, and Bayesian inference methods.

Reference

[1] Rebecca DerSimonian and Nan Laird. Meta-analysis in clinical trials. Controlled clinical trials, 7(3):177–188, 1986.

[2] Rebecca DerSimonian and Raghu Kacker. Random-effects model for meta-analysis of clinical trials: an update. Contemporary clinical trials, 28(2):105–114, 2007.

Student perspectives: Extending multilevel network meta-regression to disconnected networks and single-arm studies

A post by Sam Perren, PhD student on the Compass programme.

Over the past year, my research has been focused on a method called network meta-analysis (NMA), which is widely used in healthcare decision-making to summarise evidence on the relative effectiveness of different treatments. In particular, I have been interested in the challenges presented by disconnected networks of evidence and single-arm studies and aim to extend the multinma package to handle these challenges. Recently, I presented at the International Society for Clinical Biostatistics (ISCB) conference in Thessaloniki, Greece. In this blog post, I will outline the key points from that presentation and discuss the latest developments from my research.

Network meta-analysis

Network Meta-Analysis (NMA) pools summary treatment effects from randomised control trials (RCTs) to estimate relative effects between multiple treatments [1]. NMA summarises all direct and indirect evidence about treatment effects, allowing comparisons to be made between all pairs of treatments [2]. Covariates such as age, biomarker status, or disease severity can be either Effect Modifiers that interact with treatment effects, or Prognostic Factors that predict outcomes without interacting with treatment effects[3]. NMA requires a connected network, either directly or indirectly, through a series of comparisons[4]. Plot 1 demonstrates the assumption in NMA of constancy of relative effects, that is, the AB effect observed in study AB would be exactly the same in study AC, if a B arm had been included. However, this assumption can break down if there are differences in effect modifiers between studies which can lead to bias.[6].

Population adjustments & IPD network meta-regression

Population adjustment methods aim to relax the assumption of constancy of relative effects using available individual level data (IPD) to adjust for differences between study populations[3]. A network where IPD is available from every study enables the use of IPD network meta-regression and is considered the gold standard. However, having all IPD data in a network is rare; some studies may only provide aggregate data (AgD) in published papers.

Multilevel – Network Meta-Regression

Multilevel Network Meta-Regression (ML-NMR) is a population adjustment method that extends the NMA framework to synthesise mixtures of IPD and AgD. ML-NMR can produce estimates from networks of any size and for any given target population. It does this by first defining an individual-level regression model on the IPD, then it averages (integrates) each aggregate study population to form the aggregate level model using efficient and general numerical integration. [5]

Disconnected networks

Healthcare policymakers are increasingly encountering disconnected networks of evidence, which often include studies without control groups (single-arm studies)[6]. Very strong assumptions are required to make comparisons in a disconnected network; such as adjusting for all prognostic factors and all effect modifiers, which may not always be feasible with the available data. Current methods to handle disconnected networks include unanchored Matching-Adjusted indirect comparisons (MAIC)[7] and simulated treatment comparison (STC)[8]. However, these methods have limitations: they cannot generate estimates for target populations outside the network of evidence that might be relevant to decision makers and they are limited to a two study-scenario. So there remains a need for more flexible and robust methods, such as an extended version of the ML-NMR approach, to better handle disconnected networks of evidence.

Example: Plaque Psoriasis

We use a network of 6 active treatments plus placebo all used to treat moderate-to-severe plaque psoriasis, previously analysed by Philippo et al. [9]. In this network, we have AgD from the following studies: CLEAR, ERASURE, FEATURE, FIXTURE, and JUNCTURE. Additionally, we have IPD from the IXORA-S, UNCOVER-1, UNCOVER-2, and UNCOVER-3 studies. Outcomes of interest include success/failure to achieve at least 75%, 90% or 100% improvement on the Psoriasis Area and Severity Index (PASI) scale at 12 weeks compared to baseline, denoted PASI 75, PASI 90, and PASI 100, respectively. We make adjustments for potential effect modifiers, including duration of psoriasis, previous systemic treatment, body surface area affected, weight, and psoriatic arthritis.

This network (Plot 2) of evidence is connected; every pair of treatments is joined by a path of study comparisons. We will now disconnect this network to illustrate different methods for reconnecting using ML-NMR, and then compare the results back to the “true” results from the full evidence network. We removed the CLEAR study and removed the placebo arms from the ERASURE, FEATURE, and JUNCTURE studies, as well as the Secukinumab 150 mg and Secukinumab 300 mg arms from the FIXTURE study in the AgD. $N_1$ (Left hand side) shows studies comparing different doses of Secukinumab, 150mg and 300mg, $N_2$ shows studies comparing all other treatments. We are then faced with the challenge of wanting to make valid comparisons between treatments in these two sub-networks, illustrated in Plot 3.

Reconnected network – internal evidence

One approach is to combine two AgD studies from opposite sides of the network into a single study. The Fixture study is the only AgD study in $N_2$. To determine the appropriate study to combine with in $N_1$, aggregate-level matching is used[10]. This involves selecting the study that minimises the Euclidean distance between the observed sets of covariates. Table 1 shows the Erasure study has the most similar characteristics to Fixture. As a result, these two studies will be combined into a new four-arm study, referred to as FIXTURE/ERASURE, effectively bridging the gap in the network.

Reconnected network – external evidence

Another method we used to reconnect the network is by incorporating external observational studies, specifically “Chiricozzi” and “Prospect,” which observe the effects of Secukinumab 300mg. We incorporated these single-arm studies into the Fixture study as if they were part of the original trial, thereby effectively bridging the network. As a result, we end up with two separate reconnected networks, each using one of the observational studies.

Producing Population-Average Estimates

We have four networks for comparison: Full connected network, Reconnected using single arm study (Chircozzi), Reconnected using single arm study (Prospect), Reconnected using aggregate-level matching (FIXTURE/ERASURE). For each network, we will run both ML-NMR and standard NMA without regression. These analyses will produce population-adjusted relative treatment effects and probability outcomes for achieving a 75% reduction in the Plaque Area Severity Index (PASI75).

The ML-NMR results in the fully connected network will serve as the gold standard. We will compare the results obtained from the different methods (ML-NMR vs. NMA) and across the various networks (Full vs. reconnected) to evaluate the impact of different approaches on the relative treatment effects and outcome probabilities.

Relative Effects vs Placebo

Plot 6 shows the probit relative treatment effects versus placebo across three populations: Feature ($N_1$), Uncover-1 ($N_2$), and the external population, Prospect. The results demonstrate that for treatments in $N_2$, the estimates produced by both NMA and ML-NMR are generally close to the gold standard. This similarity between NMA and ML-NMR is largely due to the homogeneity of the populations within the networks and the limited covariates we used to match original analysis. However, NMA results show smaller confidence intervals compared to ML-NMR, which may suggest an overconfidence in the NMA model’s results. ML-NMR accounts for more complexity and variability therefore extrapolates results.

For the Prospect population, the NMA results exhibit slight bias, likely due to differences between the external population and the network populations.

Results for treatments in $N_1$ show varying degrees of accuracy when compared to the gold standard in all populations. Among the reconnected networks, the FIXTURE/ERASURE and Prospect reconnected networks perform relatively well, while the Chiricozzi-based network struggles to match the gold standard results. This is due to Chiricozzi differing the most on covariates compared to all other populations.

In other words, when comparisons are made across the created “bridges” in the reconnected networks, bias can be introduced into our results.

The plot above is the reconnected plot using PROSPECT and Chiricozzi external studies and shows us what we mean by comparisons across the “bridge”. All results in plot (1) are relative to a placebo (PBO) which is in $N_2$. If we want to make comparisons to the placebo with treatments from $N_1$ we will need to use these generated direct comparisons or “bridges”.

Absolute probability of PASI75

In Plot 8, the FEATURE population results are very close to the gold standard for treatments in $N_1$ but results for treatments in $N_2$ show some bias. Unlike in the probit differences, the reference treatment for FEATURE now become Secukinumab 150mg and 300mg (SEC_150 & SEC_300) so in order to estimate absolute outcomes for $N_2$ treatments, we need to use our “bridges”, thereby incurring bias. This narrative is the same for the other 2 population estimates, where UNCOVER-2 is in $N_2$, estimates for treatments in $N_1$ are bias compared to the gold standard, dependent on network used. For PROSPECT, it’s reference treatment is Secukinumab 150mg ($N_1$), therefore results for $N_2$ treatments vary from the gold standard.

Key Findings

When producing estimates across reconnected networks, there’s a risk that the estimates may be biased or deviate from the true value. In our analysis, reconnecting the networks using ML-NMR showed little improvement over NMA. These results highlight the importance of carefully selecting studies to bridge networks and minimise bias. As disconnected networks become more common, it’s clear that better tools for evidence synthesis are needed to ensure reliable results that can inform clinical decisions and improve outcomes.

Future Work

To improve the performance of ML-NMR over NMA, we will try incorporating more covariates into the regression model. We also plan to conduct a comprehensive simulation study to compare methods under various scenarios and explore additional approaches, such as class effects. Developing methods to assess the strong assumptions required for reconnecting networks will be another priority. Finally, we aim to implement these methods within the multinma package.

References

[1] – Sofia Dias, Anthony E Ades, Nicky J Welton, Jeroen P Jansen, and Alexander J Sutton. Network meta-analysis for decision-making. John Wiley & Sons, 2018.

[2] – Song F, Altman DG, Glenny AM, Deeks JJ. Validity of indirect comparison for estimating efficacy of competing interventions: empirical evidence from published meta-analyses. Bmj. 2003 Mar 1;326(7387):472.

[3] – David M Phillippo, Anthony E Ades, Sofia Dias, Stephen Palmer, Keith R Abrams, and Nicky J Welton. Methods for population-adjusted indirect comparisons in health technology appraisal. Medical decision making, 38(2):200–211, 2018

[4] – Sofia Dias, Alex J Sutton, AE Ades, and Nicky J Welton. Evidence synthesis for decision making 2: a generalized linear modeling framework for pairwise and network meta-analysis of randomized controlled trials. Medical Decision Making, 33(5):607–617, 2013

[5] – David M Phillippo, Sofia Dias, AE Ades, Mark Belger, Alan Brnabic, Alexander Schacht, Daniel Saure, Zbigniew Kadziola, and Nicky J Welton. Multilevel network meta-regression for population- adjusted treatment comparisons. Journal of the Royal Statistical Society. Series A,(Statistics in Society), 183(3):1189, 2020

[6] – John W Stevens, Christine Fletcher, Gerald Downey, and Anthea Sutton. A review of methods for comparing treatments evaluated in studies that form disconnected networks of evidence. Research synthesis methods, 9(2):148–162, 2018

[7] – Signorovitch, James E., et al. “Matching-adjusted indirect comparisons: a new tool for timely comparative effectiveness research.” Value in Health 15.6 (2012): 940-947.

[8] – Caro JJ, Ishak KJ. No head-to-head trial? Simulate the missing arms. Pharmacoeconomics. 2010;28(10):957–67.

[9] – David M Phillippo, Sofia Dias, AE Ades, Mark Belger, Alan Brnabic, Daniel Saure, Yves Schy-mura, and Nicky J Welton. Validating the assumptions of population adjustment: application of multilevel network meta-regression to a network of treatments for plaque psoriasis. Medical Decision Making, 43(1):53–67, 2023

[10] – Leahy, Joy, et al. “Incorporating single‐arm evidence into a network meta‐analysis using aggregate level matching: assessing the impact.” Statistics in medicine 38.14 (2019): 2505-2523.

Student Perspectives: Bayesian LLM Finetuning

A post by Sam Bowyer, PhD student on the Compass programme.

Training large AI models is tricky business. First you’ll want to raise money — and lots of it. (OpenAI’s GPT-4 reportedly cost over $100 million to train, roughly equivalent to 0.5% of Bristol’s GDP.) With that money you’ll need to buy hardware (25,000 NVIDIA A100 GPUs should do), hire a team of talented engineers, and purchase licensing to vast quantities of data (though you might consider foregoing that last one and just hope no one complains…). Once you’ve collected enough data (say, ~13 trillion tokens-worth1), settled on a model architecture with hundred of billions, if not trillions, of parameters (each taking up at least a byte of memory), you can sit back and wait around for 100 days whilst your engineers firefight software and hardware crashes to steer your model’s training to completion.2

But for those of us who can’t afford the $10^{25}$ FLOPs (floating point operations) needed to train such a model (or who might want to avoid the associated environmental costs), what can we do? The answer lies in finetuning: taking one of the available pretrained ‘foundation’ models (such as ChatGPT, or an open source model such as one from Meta’s Llama series) and tweaking them to suit your own purposes.

The basic idea is this: these foundation models are great multitaskers, they’ve been trained well enough to generate reasonable outputs to a wide variety of inputs, but if you’re only interested in using them on a particular set of data ($\mathcal{D}_\text{finetune}$), or for a particular task, then it might be a good idea to spend some extra time training on that data specifically, after the rest of (pre)training has taken place. Similarly, it’s worth noting that the foundation model you get straight out of pretraining will mimic its input dataset, $\mathcal{D}$. In the case that $\mathcal{D}$ is too large to be checked by humans (e.g. 13 trillion tokens — essentially including most of the public internet), your model will almost certainly have learnt undesirable behaviour and be capable of producing dangerous, offensive, and harmful output. Finetuning is critical to the pursuit of safe AI, putting guardrails in place and ensuring that a model’s behaviour is aligned with our desires, both in terms of utility and safety.3

In this blog post, I’ll give an overview of LLM finetuning, specifically parameter-efficient finetuning, which tackles the problem of finetuning models whilst avoiding the computational burden that was required for pretraining. Even if your finetuning dataset $\mathcal{D}_\text{finetune}$ is much smaller than your pretraining set $\mathcal{D}$, you’ve still got the computational problem of the model’s size: how do you efficiently4 do gradient-based optimisation on a model with potentially billions of parameters? I’ll also argue that taking a Bayesian approach can be beneficial, and that whilst the added computational cost of Bayes might not be feasible (or even all that helpful) in the pretraining setting, these costs are much less impactful when finetuning.

Parameter Efficient Finetuning

Perhaps the simplest way to finetune a model on $\mathcal{D}_\text{finetune}$ is to simply carry on training as before — with some gradient-based optimiser like Adam [1] — but on this new dataset (often repeatedly, i.e. for multiple ‘epochs’). This is known as full finetuning (FFT) and usually leads to the best results, however, it’s often infeasible due to the size of the model being finetuned.

Recall that the model we’re working with might have billions of parameters — in order to train these parameters we need to store not only their values, but also their gradients, as well as the activation values of each neuron in the network and, depending on your optimiser, potentially momentum and second order gradient information (e.g. Adam makes use of the exponential moving average of gradients and the EMA of squared gradients — all per parameter). On a model like Llama-7B, whose 7 billion parameters at 8-bit precision require 7GB of storage, these extra gradient costs can easily overwhelm the 16GB capacity of a typical high-end consumer GPU such as an NVIDIA RTX 4080. (Add to that the fact that we usually want to batch our input data — that is, pass multiple input examples through the model at a time — and you can see where things start to spiral out of control.)

This motivates the need for finetuning algorithms that have a smaller memory footprint. There’s an exciting field of literature in model compression and quantisation — using compression techniques to represent your model and its gradients by fewer and fewer bits5, but another approach is to simply reduce the number of parameters that you train during finetuning. However, choosing which parameters to train and which to freeze (thus freeing up space that would’ve gone to storing the gradient information of those parameters) is far from trivial.

Partial Finetuning

In order to discuss finetuning techniques, it’ll be useful to briefly touch on the basic architecture of neural networks. The simplest type of neural network is a multilayer perceptron, or MLP, which consists of $L$ layers in which the output of layer $l-1$, $x^{l-1} \in \mathbb{R}^{d_{l-1}}$, is multiplied by a learnable weight matrix $W^l \in \mathbb{R}^{d_{l} \times d_{l-1}}$ and added to a learnable bias vector $b^l \in \mathbb{R}^{d_{l}}$ before being transformed through a nonlinearity, such as a sigmoid $\sigma(x) = (1+e^{-x})^{-1}$:

$$x^l = \sigma(W^l x^{l-1} + b^l),$$

with $x^0 \in \mathbb{R}^{d_0}$ being input data.

A common strategy for finetuning is to freeze all weights in earlier layers, say, up until the final $\hat{L}$ layers, and only train the set of parameters $\{W^l, b^l | l \geq L-\hat{L}\}$. Assuming constant network width $d = d_0 = \ldots = d_L$ this reduces the number of trainable parameters from $L(d^2 + d)$ to $\hat{L}(d^2 + d)$.

Another simple finetuning strategy is BitFit [3], which works by only training the bias parameters, leading to a total of $Ld$ trainable parameters (though of course this does make the iterative finetuning updates significantly less expressive).

It’s important to note that the final-layers-only approach can also be applied more generally. Most LLMs architectures use transformers [4] as their backbone, which — very loosely speaking — consist of multi-headed attention layers (another, more complicated type of neural network) followed by an MLP (plus a whole bunch of other stuff containing yet more parameters), and with each transformer’s output typically going on to form the input of another transformer. So it’s common to see only the final transformer finetuned, or even only the final transformer’s MLP.

Since it would be ill-advised to take a long detour into the definition of multi-headed attention here (as that’d be fairly involved and might take the momentum out of our finetuning discussion), I won’t do that. (Instead, I’ll banish it to yet another (increasingly-obnoxious) footnote6.)

Adapter Tuning

Rather than retraining the weights already in your model, most modern finetuning approaches actually add new parameters to the model, termed ‘adapters’, and only train these instead. For example, [5], [6], and [7] all essentially propose techniques in which we insert two-layer MLPs at different places inside a transformer, with varying results.

Adapter methods have the benefit of being ‘plug-and-play’, in the sense that you can train multiple adapters on different finetuning tasks and then insert them into your model if you detect that it would be helpful for a user’s given request.

Low Rank Adaptation (LoRA)

By far the most common (and almost de facto standard as of 2024) finetuning method is Low Rank Adaptation (LoRA) [8]. The intuition behind LoRA is that the parameters inside your pretrained model are probably fairly close to their finetuned optimal values already, in the sense that those optimal values can probably be reached using only updates in a low-rank subspace. As such we can pose our finetuning problem in terms of finding the low-rank matrix $\Delta W \in \mathbb{R}^{d_\text{in} \times d_\text{out}}$ that optimises a given pretrained weight matrix $W_0$, leading to

$$W_\text{finetune} = W_0 + \Delta W,$$

where the low-rank of $\Delta W$ is enforced by parameterising it as $$\begin{aligned}\Delta W & = B A \\ B & \in \mathbb{R}^{d_\text{in} \times r} \\ A & \in \mathbb{R}^{r \times d_\text{out}} \end{aligned}$$so that $\text{rank}(\Delta W) \leq r \ll \text{rank}(W_0) \leq \min (d_\text{in}, d_\text{out})$. (Note that LoRA places the adapter in parallel to a pretrained weight matrix $W_0$, in contrast to the serial/in-between placement of the MLP adapters mentioned in the previous section.)

LoRA’s success has led to a large number of variants, such as AdaLoRA [9] which adaptively decides which weight matrices to apply LoRA to based on their singular values. Other methods include PiSSA (Principal Singular Values and Singular Vectors Adaptation) [10] which performs LoRA updates only on the first few principle components of each weight matrix and freezes the ‘residuals’ which come from later principle components. One recent paper presents GaLore (Gradient Low Rank Projection) [11], which performs PCA on the weight matrix every few iterations and performs low-rank updates by specifically only optimising in the (low-rank) space spanned by the first few priniciple components.

Bayesian Finetuning

Although work has been done to introduce uncertainty estimation into pretraining, the results often aren’t worth the extra computational costs [12, 13]. Not only are the model sizes too large to make uncertainty quantification feasible, but the fact that your pretraining dataset, $\mathcal{D}$, is gigantic provides little uncertainty to reason about. However, in the context of finetuning we typically have a much smaller dataset, for which we’ll likely have much more uncertainty, and we also tend to work with far fewer parameters, allowing for extra computational budget to go towards the use of Bayesian methods.

Consider splitting up our finetuning set into prompt and target/response pairs $(X,y) \in \mathcal{D}_\text{finetune}$ where $X \in \mathcal{T}^{B \times n}$ is a matrix of $B$ sequences each of maximum length $n$ (potentially padded out with null-tokens) constructed with the token set $\mathcal{T}$, and $y \in \mathcal{Y}^B$ could be a corresponding batch of single tokens (in which case $\mathcal{Y} = \mathcal{T}$), or a batch of classification labels (e.g. in sentiment analysis, or multiple-choice Q&A, in which case $\mathcal{Y}$ might be different to $\mathcal{T}$).

What we fundamentally want to learn is a posterior distribution over all learnable parameters $$p(\theta | \mathcal{D}_\text{finetune}) = p(\theta | X, y),$$where, for example, in the case of LoRA finetuning, $\theta$ is the collection of all adapter weights $A$ and $B$. This not only gives us information about the uncertainty in the model’s parameters, which can be useful in itself, but can also be used to give us the posterior predictive distribution for a test input $x^* \in \mathcal{T}^n$, $$p(y^* | x^*, \mathcal{D}_\text{finetune}) = \int p(y^* | x^*, \theta)p(\theta|\mathcal{D}_\text{finetune})d\theta.$$

This is often more desirable than a predictive distribution that only uses a point estimate of $\theta$ and which would then ignore the uncertainty present in the model’s parameters.

Bayesian LoRA (via Laplace Approximation and KFAC)

Yang et al. [14] suggest a method for finding the posterior $$p(\theta | X, y) \propto p(y | X, \theta)p(\theta)$$post-hoc, i.e. after regular finetuning (with LoRA) using a Laplace approximation — which assumes the posterior is a Gaussian centered at the maximum a-posteriori (MAP) solution, $\theta_\text{MAP}$.

First, we note that the MAP solution can be written as the maximum of the log-joint $\mathcal{L}(y, X; \theta)$, $$\begin{align} \mathcal{L}(y, X; \theta) &= \log p(y | X, \theta) +\log p(\theta) = \log p(\theta | X, y) + \text{const} \\ \theta_\text{MAP} &= \arg\max{}_\theta \mathcal{L}(y, X; \theta). \end{align}$$

Then assuming that the finetuning successfully optimised $\theta$, i.e. reached parameter values $\theta_\text{MAP}$, the Laplace approximation involves taking the second-order Taylor expansion of the log-joint around $\theta_\text{MAP}$, $$\mathcal{L}(y, X; \theta) \approx \mathcal{L}(y, X; \theta_\text{MAP}) – \frac{1}{2}(\theta – \theta_\text{MAP})^T(\nabla_\theta^2 \mathcal{L}(X, y; \theta)|_{\theta_\text{MAP}})(\theta – \theta_\text{MAP}).$$(The expansion’s first-order term disappears because the gradient of the MAP objective at $\theta_\text{MAP}$ is zero.) This quadratic form can then be written as a Gaussian density, with mean $\theta_\text{MAP}$ and covariance given by the inverse of the log-joint Hessian: $$\begin{align}p(\theta | X, y) &\approx \mathcal{N}(\theta ; \theta_\text{MAP}, \Sigma), \\

\Sigma &= -(\nabla_\theta^2 \mathcal{L}(X, y; \theta))^{-1}.\end{align}$$

The authors makes use of various tricks to render computing this Hessian inverse feasible, most notably Kronecker-Factored Approximate Curvature (KFAC) [15]. (A nice explanation of which can be found at this blog post.)

Using the Laplace approximation comes with added benefits. Specifically, we can make use of the Gaussian form of the (approximate) posterior to easily compute two values of interest: samples from the posterior predictive distribution, and estimates of the marginal likelihood.

For the first of these, we can linearise our model, with output $f_\theta(x^*)$ approximated by a first-order Taylor expansion around $\theta_\text{MAP}$, $$f_\theta(x^*) \approx f_{\theta_\text{MAP}}(x^*) + \nabla_\theta f_\theta(x^*)|^T_{\theta_\text{MAP}}(\theta – \theta_\text{MAP}).$$

We can write this as a Gaussian density $$f_\theta(x^*) \sim \mathcal{N}(y^*; f_{\theta_\text{MAP}}(x^*), \Lambda)$$ where $$\Lambda = (\nabla_\theta f_\theta(x^*)|^T_{\theta_\text{MAP}})\Sigma(\nabla_\theta f_\theta(x^*)|_{\theta_\text{MAP}}).$$

With this, we can easily obtain samples from our predictive posterior through reparameterised sampling of some Gaussian noise $\mathbf{\xi} \sim \mathcal{N}(\mathbf{0}, \mathbf{I})$ and a Cholesky decomposition $\Lambda = LL^T$: $$\hat{y} = f_\theta(x^*) = f_{\theta_\text{MAP}}(x^*) + L\mathbf{\xi}.$$

The second value of interest is the marginal likelihood (also known as the model evidence), which is useful for hyperparameter optimisation and can be computed simply as follows $$\begin{align}p(y|X) &= \int p(y|X,\theta)p(\theta)d\theta \\ &\approx \exp (\mathcal{L}(y, X; \theta_\text{MAP}))(2\pi)^{D/2}\det(\Sigma)^{1/2}.\end{align}$$

Using Stein Variational Gradient Descent (SVGD)

A reasonable question to ask is whether it might be feasible to learn the posterior distribution during finetuning, rather than afterwards. One such method for achieving this is Stein variational gradient descent (SVGD) [16], in which a collection of $n$ parameter particles $\{\theta_i^{(0)}\}_{i=1}^n$ are iteratively updated to fit the true posterior using some similarity function (i.e. a kernel) $k: \Theta \times \Theta \to \mathbb{R}$, $$\begin{align}\theta_i^{t+1} &= \theta_i^{(t)} – \epsilon_i \phi(\theta_i^{(t)}) \\ \phi(\theta_i) &= \frac{1}{n} \sum_{j=1}^n \left[\frac{1}{T}k(\theta_j,\theta_i)\nabla_{\theta_j}\log p(\theta_j | \mathcal{D}_\text{finetune}) + \nabla_{\theta_j} k(\theta_j, \theta_i) \right],\end{align}$$where $\epsilon_i$ is a learning rate and $T$ is a temperature hyperparameter. The basic interpretation of the update is that the first term inside the summation drives particles towards areas of high posterior probability, whilst the second term penalises particles that are too similar to one another, acting as a repulsive force that encourages exploration of the parameter-space.

Once the particles have converged, we can simply approximate the posterior predictive as the average output of the network across each parameter particle $\theta_i$, $$p(y^* | x^*, \mathcal{D}_\text{finetune}) \approx \frac{1}{n} \sum_{i=1}^n f_{\theta_i}(x^*).$$

My current research lies in applying SVGD to LoRA adapters. The hopes are that we can learn a richer, multi-modal posterior distribution using SVGD’s particles without making the Gaussian posterior assumption of the Laplace approximation. Recent concurrent work [17] applies a very similar technique to computer-vision tasks and achieves promising results.

Conclusion

I hope this blog has been a useful introduction to the finetuning of LLMs. Feel free to get in touch if you’re interested! My email is sam.bowyer@bristol.ac.uk.

Footnotes

1: LLMs split input text up into a sequence of tokens. Roughly speaking, most words are split into one or two tokens depending on how common and how long they are. Using GPT-4’s tokenizer, this sentence is made from 17 tokens. (back to top)

2: Spare a moment, if you will, for the Meta engineers behind the OPT-175B (175 billion-parameters) model. The training logbook of which reads at times like that of a doomed ship at sea. (back to top)

3: Note that in the case of LLMs specifically, the straight-out-of-pretraining model will also likely be a poor virtual assistant, in the way we tend to desire of chatbots like ChatGPT. A model which can complete sentences to match the general patterns found in $\mathcal{D}$ won’t necessarily be much good at the user-agent back-and-forth conversation style we’d like, and as such might not have properly ‘learnt’ how to, for example, follow instructions and answer questions. It’s because of this that most public-facing LLMs go through what’s known as instruction fine-tuning, in which the model is finetuned on a large dataset of instruction-following chat logs before being deployed. (back to top)

4: That is, without using 25,000 GPUs… (back to top)

5: Consider this paper [2] by Huang et al. which boasts 1.08-bit quantisationa of 16-bit models, all whilst retaining impressive levels of performance. (back to top)

a : i.e. representing parameters with an average precision of 1.08 bits.

6:

An (Ill-Advised) Aside: Attention

Attention layers work by taking three matrices as input, $Q_\text{input}, K_\text{input}, V_\text{input} \in \mathbb{R}^{n \times d_\text{model}}$, typically representing $d_\text{model}$-dimensional embeddings of a sequence of $n$ tokens. First we project these matrices using learnable weight matrices $W^Q, W^K \in \mathbb{R}^{d_\text{model} \times d_k}$, and $W^V \in \mathbb{R}^{d_\text{model} \times d_v}$ to obtain our queries, keys and values: $$\begin{align}

Q &= Q_\text{input} W^Q \in \mathbb{R}^{n \times d_k} \\

K &= K_\text{input} W^K \in \mathbb{R}^{n \times d_k} \\

V &= V_\text{input} W^V \in \mathbb{R}^{n \times d_v}.

\end{align}$$With these, we then compute attention as $$\text{Attention}(Q, K, V) = \text{softmax}\left(\frac{QK^T}{\sqrt{d_k}}\right)V$$ where $\text{softmax}$ is applied over each row such that, denoting the $i$th row of the matrix $A = QK^T$ as $A^{(i)}$ and that row’s $j$th element as $a^{(i)}_j$, we define: $$\text{softmax}(A)^{(i)} = \frac{\exp A^{(i)}}{\sum_{j=1}^n \exp a^{(i)}_j}.$$

The intuition behind this is that our $n \times n$ attention matrix $\text{softmax}(QK^T/\sqrt{d_k})$ has entries representing how much token $i$ relates (or ‘attends’) to token $j$. The $\text{softmax}$ normalises each row so that the entries all add up to one, allowing us to think of each row as a distribution over tokens. The final multiplication with $V$ might then be thought of as selecting (or weighting) tokens in $V$ according to those distributions.

One important limitation of the attention mechanism we’ve just described is that it only allows us to consider how each token attends to each other token in some universal way, whereas in reality there are multiple ways that words in a sentence (for example) can relate to each other. Because of this, most of the time we actually use multi-headed attention, in which we compute attention between the token sequences $H \in \mathbb{N}$ times, each time with different learnable weight matrices $W^Q_h, W^K_h, W^V_h$ for $h \in \{1,\ldots,H\}$. Then we combine these separate attention heads, using yet another learnable weight matrix $W^O \in \mathbb{R}^{H d_v \times d_\text{model}}$, $$\text{MultiHead}(Q_\text{input}, K_\text{input}, V_\text{input}) = \text{Concat}(\text{head}_1,\ldots,\text{head}_H)W^O \in \mathbb{R}^{n \times d_\text{model}},$$ where $\text{head}_h = \text{Attention}(Q_\text{input}Q_h, K_\text{input}K_h, V_\text{input}V_h)$. Allowing the model to learn different types of attention on different heads makes MHA an incredibly powerful and expressive part of a neural network.

To summarise and return to the discussion of finetuning: MHA layers contain a ton of learnable parameters (specifically, $2H d_\text{model} (d_k + d_v)$ of them). (back to top)

References

[1] Kingma, D.P., 2014. Adam: a method for stochastic optimization. arXiv preprint arXiv:1412.6980.

[2] Huang, W., Liu, Y., Qin, H., Li, Y., Zhang, S., Liu, X., Magno, M. and Qi, X., 2024. Billm: Pushing the limit of post-training quantization for llms. arXiv preprint arXiv:2402.04291.

[3] Zaken, E.B., Ravfogel, S. and Goldberg, Y., 2021. Bitfit: Simple parameter-efficient fine-tuning for transformer-based masked language-models. arXiv preprint arXiv:2106.10199.

[4] Vaswani, A., 2017. Attention is all you need. arXiv preprint arXiv:1706.03762.

[5] Houlsby, N., Giurgiu, A., Jastrzebski, S., Morrone, B., De Laroussilhe, Q., Gesmundo, A., Attariyan, M. and Gelly, S., 2019, May. Parameter-efficient transfer learning for NLP. In International conference on machine learning (pp. 2790-2799). PMLR.

[6] Lin, Z., Madotto, A. and Fung, P., 2020. Exploring versatile generative language model via parameter-efficient transfer learning. arXiv preprint arXiv:2004.03829.

[7] Pfeiffer, J., Kamath, A., Rücklé, A., Cho, K. and Gurevych, I., 2021. AdapterFusion: Non-Destructive Task Composition for Transfer Learning. EACL 2021.

[8] Hu, E.J., Shen, Y., Wallis, P., Allen-Zhu, Z., Li, Y., Wang, S., Wang, L. and Chen, W., 2021. Lora: Low-rank adaptation of large language models. arXiv preprint arXiv:2106.09685.

[9] Zhang, Q., Chen, M., Bukharin, A., Karampatziakis, N., He, P., Cheng, Y., Chen, W. and Zhao, T., 2023. AdaLoRA: Adaptive budget allocation for parameter-efficient fine-tuning. arXiv preprint arXiv:2303.10512.

[10] Meng, F., Wang, Z. and Zhang, M., 2024. Pissa: Principal singular values and singular vectors adaptation of large language models. arXiv preprint arXiv:2404.02948.

[11] Zhao, J., Zhang, Z., Chen, B., Wang, Z., Anandkumar, A. and Tian, Y., 2024. Galore: Memory-efficient llm training by gradient low-rank projection. arXiv preprint arXiv:2403.03507.

[12] Cinquin, T., Immer, A., Horn, M. and Fortuin, V., 2021. Pathologies in priors and inference for Bayesian transformers. arXiv preprint arXiv:2110.04020.

[13] Chen, W. and Li, Y., 2023. Calibrating transformers via sparse gaussian processes. arXiv preprint arXiv:2303.02444.

[14] Yang, A.X., Robeyns, M., Wang, X. and Aitchison, L., 2023. Bayesian low-rank adaptation for large language models. arXiv preprint arXiv:2308.13111.

[15] Martens, J. and Grosse, R., 2015, June. Optimizing neural networks with kronecker-factored approximate curvature. In International conference on machine learning (pp. 2408-2417). PMLR.

[16] Liu, Q. and Wang, D., 2016. Stein variational gradient descent: A general purpose bayesian inference algorithm. Advances in neural information processing systems, 29.

[17] Doan, B.G., Shamsi, A., Guo, X.Y., Mohammadi, A., Alinejad-Rokny, H., Sejdinovic, D., Ranasinghe, D.C. and Abbasnejad, E., 2024. Bayesian Low-Rank LeArning (Bella): A Practical Approach to Bayesian Neural Networks. arXiv preprint arXiv:2407.20891.

Student Perspectives: Factor-adjusted vector autoregressive models

A post by Dylan Dijk, PhD student on the Compass programme.

Introduction

My current project is looking to robustify the performance of time series models to heavy-tailed data. The models I have been focusing on are vector autoregressive (VAR) models, and additionally factor-adjusted VAR models. In this post I will not be covering the robust methodology, but will be introducing VAR models and providing the motivation for introducing the factor adjustment step when working with high-dimensional time series.

Vector autoregressive models

In time series analysis the objective is often to forecast a future value given past data, for example, one of the classical models for univariate time series is the autoregressive AR(d) model:

\[X_t = a_1 X_{t-1} + \dots + a_d X_{t-d} + \epsilon_t \, .\]

However, in many cases, the value of a variable is influenced not just by its own past values but also by past values of other variables. For example, in Economics, household consumption expenditures may depend on variables such as income, interest rates, and investment expenditures, therefore we would want to include these variables in our model.

The VAR model [1] is simply the multivariate generalisation of the univariate autoregressive model, that is, for a $p$-dimensional stochastic process $(\dots, \mathbf{X}_t, \mathbf{X}_{t+1}, \dots) \in \mathbb{R}^p$ we model an observation at time $t$ as a linear combination of previous observations up to some lag $d$ plus an error:

\[\mathbf{X}_t = \mathbf{A}_1 \mathbf{X}_{t-1} + \dots + \mathbf{A}_d \mathbf{X}_{t-d} + \boldsymbol{\epsilon}_t \, ,\]

where $\mathbf{A}_i$ are $p \times p$ coefficient matrices. Therefore, in addition to modelling serial dependence, the model takes into account cross-sectional dependence. This model can then be used for forecasting, and as an explanatory model to describe the dynamic interrelationships between a number of variables.

Estimation

Given a dataset of $n$ observations, $\{\mathbf{X}_1, \dots, \mathbf{X}_n \in \mathbb{R}^p\}$, we can aim to estimate the coefficient matrices. In order to do so, the model can be written in a stacked form:

\begin{align*} \underbrace{\left[\begin{array}{c}\left(\mathbf{X}_n\right)^{T} \\ \vdots \\ \left(\mathbf{X}_{d+1}\right)^{T}\end{array}\right]}_{\boldsymbol{\mathcal{Y}}} & =\underbrace{\left[\begin{array}{ccc}\left(\mathbf{X}_{n-1}\right)^{T} & \cdots & \left(\mathbf{X}_{n-d}\right)^{T} \\ \vdots & \ddots & \vdots \\ \left(\mathbf{X}_{d}\right)^{T} & \cdots & \left(\mathbf{X}_1\right)^{T}\end{array}\right]}_{\boldsymbol{\mathcal{X}}} \underbrace{\left[\begin{array}{c}\boldsymbol{A}_1^{T} \\ \vdots \\ \boldsymbol{A}_d^{T}\end{array}\right]}_{\boldsymbol{A}^T}+\underbrace{\left[\begin{array}{c}\left(\boldsymbol{\epsilon}_n\right)^{T} \\ \vdots \\ \left(\boldsymbol{\epsilon}_d\right)^{T}\end{array}\right]}_{\boldsymbol{E}}

\end{align*}

and subsequently vectorised to return a standard univariate linear regression problem

\begin{align*}

\operatorname{vec}(\boldsymbol{\mathcal{Y}}) & =\operatorname{vec}\left(\boldsymbol{\mathcal{X}} \boldsymbol{A}^T\right)+\operatorname{vec}(\boldsymbol{E}), \\ & =(\textbf{I} \otimes \boldsymbol{\mathcal{X}}) \operatorname{vec}\left(\boldsymbol{A}^T\right)+\operatorname{vec}(\boldsymbol{E}), \label{eq:stacked_var_regression_form}\\ \underbrace{\boldsymbol{Y}}_{N p \times 1} & =\underbrace{\boldsymbol{Z}}_{N p \times q} \underbrace{\boldsymbol{\beta}^*}_{q \times 1}+\underbrace{\operatorname{vec}(\boldsymbol{E})}_{N p \times 1}, \quad N=(n-d), \quad q=d p^2.

\end{align*}

Sparse VAR

There are $dp^2$ parameters to estimate in this model, and hence VAR estimation is naturally a high-dimensional statistical problem. Therefore, estimation methods and associated theory need to hold under high-dimensional scaling of the parameter dimension. Specifically, this means consistency is shown for when both $p$ and $n$ tend to infinity, as opposed to in classical statistics where $p$ is kept fixed.

The linear model in the high-dimensional setting is well understood [2]. To obtain a consistent estimator requires additional structural assumptions in the model, in particular, sparsity on the true vector $\boldsymbol\beta^*$. The common approach for estimation is lasso, which can be motivated from convex relaxation in the noiseless setting. Consistency of lasso is well studied [3][4], with consistency guaranteed under sparsity, and restrictions on the directions in which the hessian of the loss function is strictly positive.

The well known lasso objective is given by:

\begin{align*}

\underset{{\boldsymbol\beta \in \mathbb{R}^q}}{\text{argmin}} \, \|\boldsymbol{Y}-\boldsymbol{Z} \boldsymbol\beta\|_{2}^{2} + \lambda \|\boldsymbol\beta\|_1 \, ,

\end{align*}

and below, we give a simplified consistency result that can be obtained under certain assumptions.

We denote the sparsity of $\boldsymbol{A}$ by

$s_{0, j}=\left|\boldsymbol\beta^*_{(j)}\right|_0, s_0=\sum_{j=1}^p s_{0, j}$ and $s_{\text {in }}=\max _{1 \leq j \leq p} s_{0, j}$.

Lasso consistency result

Suppose

\begin{gather*}

\, s_{\text{in}} \leq C_1 \sqrt{\frac{n}{\log p}} \, \; \text{and } \; \lambda \geq C_2 (\|\boldsymbol{A}^T\|_{1,\infty} + 1)\sqrt{\frac{\log p}{n}} \; ,

\end{gather*}

then with high probability we have

\begin{align*}

|\widehat{\boldsymbol{A}} – \boldsymbol{A}|_2 \leq C_3 \sqrt{s_{0}} \lambda \quad \text{and} \quad |\widehat{\boldsymbol{A}} – \boldsymbol{A}|_1 \leq C_4 s_0 \lambda \, .

\end{align*}

What we mean here by consistency, is that as $n,p \rightarrow \infty$, the estimate $\widehat{\boldsymbol\beta}$ converges to $\boldsymbol\beta$ in probability. Where we think of $p$ as being a function of $n$, so the manner in which the dimension $p$ grows depends on the sample size. For example, in the result above, we can have consistency with $p = \exp(\sqrt{n})$.

The result indicates that for larger $p$ a more sparse solution, and a larger regularisation parameter is required. Similar results have been derived under various assumptions, for instance under a Gaussian VAR the result has been given in terms of the largest and smallest eigenvalues of the spectral density matrix of a series [5], and hence consistency requires that these quantities are bounded.

In summary, for lasso estimation to work we need $\boldsymbol{A}$ to be sufficiently sparse, and the largest eigenvalue of the spectral density matrix to be bounded. But are these reasonable assumptions to make?

First two leading eigenvalues of the spectral density matrix.

Heatmap of logged p-values for evidence of non-zero coefficients after fitting ridge regression model.

Well, intuitively, if a multivariate time series has strong cross-sectional dependence we would actually expect to have many non-zero entries in the VAR coefficients $\boldsymbol{A}_i$. The figures above, taken from [6], illustrate a real dataset in which there is statistical evidence for a non-sparse solution (heatmap), and that the leading eigenvalue of the spectral density matrix diverges linearly in $p$. Therefore providing an example in which two of the assumptions discussed above are unmet.

Factor-adjusted VAR

The idea now is to assume that the covariance of the observed vector $\mathbf{X}_t$ is driven by a lower dimensional latent vector. For example, the figures above were generated from a dataset of stock prices of financial institutions, in this case an interpretation of a latent factor could be overall market movements which captures the broad market trend, or a factor that captures the change in interest rates.

\begin{align}

\mathbf{X}_t &= \underset{p \times r}{\boldsymbol\Lambda} \underset{r \times 1}{\mathbf{F}_t} + \boldsymbol\xi_t \quad

\end{align}

Consequently, first fitting a factor model would account for strong cross-sectional correlations, leaving the remaining process to exhibit the individual behaviour of each series. Fitting a sparse VAR process will now be a more reasonable choice.

In the formula above, $\mathbf{F}_t$ is the factor random vector, and $\boldsymbol\Lambda$ the constant loading matrix, which quantifies the sensitivity of each variable to the common factors, and we can model $\boldsymbol\xi_t$ as a sparse VAR process, as described in the preceding sections.

References

[1] Lütkepohl, H. (2005) New introduction to multiple time series analysis. Berlin: Springer-Verlag.

[2] Wainwright, M. (2019) High-dimensional statistics: A non-asymptotic viewpoint – Chapter 7 – Sparse linear models in high dimensions. Cambridge, United Kingdom: Cambridge University Press.

[3] Geer, Sara A. van de, and Peter Bühlmann. (2009) On the Conditions Used to Prove Oracle Results for the Lasso. Electronic Journal of Statistics. Project Euclid, https://doi.org/10.1214/09-EJS506.

[4] Bickel, Peter J., Ya’acov Ritov, and Alexandre B. Tsybakov. (2009) Simultaneous Analysis of Lasso and Dantzig Selector. The Annals of Statistics. https://doi.org/10.1214/08-AOS620.

[5] Sumanta Basu, George Michailidis. (2015) Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics. https://doi.org/10.1214/15-AOS1315.

[6] Barigozzi, M., Cho, H. and Owens, D. (2024). FNETS: Factor-adjusted network estimation and forecasting for high-dimensional time series. Journal of Business & Economic Statistics.

Student Perspectives: How can we spot anomalies in networks?

A post by Rachel Wood, PhD student on the Compass programme.

Introduction

As our online lives expand, more data than we can reasonably consider at once is collected. Many of this is sparse and noisy data, needing methods which can recover information encoded in these structures. An example of these kind of datasets are networks. In this blog post, I explain how we can do this to identify changes between networks observing the same subjects (e.g. snapshots of the same graph over time).

Problem Set-Up

We consider two undirected graphs, represented by their adjacency matrices $\mathbf{A}^{(1)}, \mathbf{A}^{(2)} \in \{0,1\}^{n \times n}$. As we can see below, there are two clusters (pink nodes form one, the yellow and blue nodes form another) in the first graph but in the second graph the blue nodes change behaviour to become a distinct third cluster.

Our question becomes, how can we detect this change without prior knowledge of the labels?

We can simply look at the adjacency matrices, but these are often sparse, noisy and computationally expensive to work with. Using dimensionality reduction, we can “denoise” the matices to obtain a $d$-dimensional latent representation of each node, which provides a natural measure of node behaviour and a simple space in which to measure change.

Graph Embeddings

There is an extensive body of research investigating graph embeddings, however here we will focus on spectral methods.

Specifically we will compare the approaches of Unfolded Adjacency Spectral Embedding (UASE) presented in [1] and CLARITY presented in [2]. Both of these are explained in more detail below.

UASE

UASE takes as input the unfolded adjacency matrix $\mathbf{A} = \left[ \mathbf{A}^{(1)}\big| \mathbf{A}^{(2)}\right] \in \{0,1\}^{2n \times n}$ and performs $d$ truncated SVD [3] to obtain a $d$-dimensional static and a $d$-dimensional dynamic representation:

Mathematically we can write this as:

\begin{equation*}

\mathbf{A} = \mathbf{U} \boldsymbol{\Sigma} \mathbf{V}^T = \mathbf{U}_{\mathbf{A}} \boldsymbol{\Sigma}_{\mathbf{A}} \mathbf{V}_{\mathbf{A}}^T + \mathbf{U}_{\perp \!\!\!\ } \ \boldsymbol{\Sigma}_{\perp \!\!\!\ } \ \mathbf{V}_{\perp \!\!\!\ }^T \ \approx \mathbf{U}_{\mathbf{A}} \boldsymbol{\Sigma}_{\mathbf{A}} \mathbf{V}_{\mathbf{A}}^T = \mathbf{X} \mathbf{Y}^T

\end{equation*}

where $\mathbf{U}_{\mathbf{A}}, \mathbf{V}_{\mathbf{A}}$ are the first $d$ columns of $\mathbf{U}$ and $\mathbf{V}$ respectively and $\boldsymbol{\Sigma}_{\mathbf{A}}$ is the diagonal matrix which forms the $d \times d$ upper left block of $\boldsymbol{\Sigma}$. This gives a static embedding $\mathbf{X} \in \mathbb{R}^{n \times d}$ and a time evolving embedding $\mathbf{Y} \in \mathbb{R}^{2n \times d}$.

The general approach in UASE literature is to measure change by comparing latent positions, which is backed by [4]. This paper gives a theoretical demonstration for longitudinal and cross-sectional stability in UASE, i.e. for observations $i$ at time $s$ and $j$ at time $t$ behaving similarly, their latent positions should be the same: $\hat Y_i^{(s)} \approx \hat Y_j^{(t)}$. This backs the general approach in the UASE literature of comparing latent positions to quantify change.

Going back to our example graphs, we apply UASE to the unfolded adjacency matrix and visualise the first two dimensions of the embedding for each of the graphs:

As we can see above, the pink nodes have retained their positions, the yellow nodes have moved a little and the blue nodes have moved the most.

CLARITY

Clarity takes a different approach, by estimating $\mathbf{A}^{(2)}$ from $\mathbf{A}^{(1)}$. An illustration of how it is done is shown below:

Again we provide a mathmatical explanation of the method. First we perform a $d$-dimensional truncated eigendecompositionon $\mathbf{A}^{(1)}$:

\begin{equation*}

\mathbf{A}^{(1)} = \mathbf{U}^{(1)} \boldsymbol{\Sigma}^{(1)} \mathbf{U}^{(1)T} + \mathbf{U}_{\perp \!\!\!\ } \ \boldsymbol{\Sigma}_{\perp \!\!\!\ } \ \mathbf{U}_{\perp \!\!\!\ }^T \ \approx \mathbf{U}^{(1)} \boldsymbol{\Sigma}^{(1)} \mathbf{U}^{(1)T} = \hat{\mathbf{A}}^{(1)}

\end{equation*}

where $\mathbf{U} \in \mathbb{R}^{n \times d}$ is a matrix of the first $d$ eigenvectors and $\Sigma \in \mathbb{R}^{d \times d}$ is a diagonal matrix with the first $d$ eigenvalues.

Then we estimate $\mathbf{A}^{(2)}$ as

\begin{equation*}

\hat{\mathbf{A}}^{(2)} = \mathbf{U}^{(1)} \boldsymbol{\Sigma }^{(2)} \mathbf{U}^{(1)T} \hspace{1cm} \text{where} \hspace{1cm} \boldsymbol{\Sigma}^{(2)} = \mathbf{U}^{(1)T} \mathbf{A}^{(2)} \mathbf{U}^{(1)}

\end{equation*}

As opposed to UASE, Clarity examines change between $\mathbf{A}^{(1)}$ and $\mathbf{A}^{(2)}$ by a quantity called persistence. These are defined as

\begin{equation*}